What's the Value of Your Digital Marketing Agency

Ryan Nead

Ryan Nead

When it comes to business valuations, beauty is not in the eye of the beholder. Value is tangible, comparable and often derived from the cost of capital, risk or the opportunity cost of the next best investment. As in marketing, it's driven by the ROI. Or, as Warren Buffett is so famous for saying:

Price is what you pay, value is what you get.

Too often business owners base their expected company valuation on things like:

- "I need $XX,XXX,XXX after tax to retire comfortably, so a buyer should be willing to pay it, because baby I'm worth it."

- "We are a company that services the unique technology sector, therefore our valuation multiple is x times greater than any standard services business"

- Facebook paid $XB for Whatsapp, Instagram or [fill in the blank]

We have worked in the buying and selling of digital services businesses and digital agency assets, including domain name valuations and acquisitions. Consequently, we know a bit about both the process of buying, how to value agencies and what it means to grow the actual true value of your agency self worth. Here we discuss all three. So, if you're looking to start a new agency, sell your SEO services agency or acquire a existing agency, there should be some helpful pointers in here from which you can glean.

How to Do Digital Agency Valuation

Digital agency owners often ask the question, "What is my digital marketing agency worth?" Unfortunately, there is no easy answer to this question. Agency valuations can vary widely depending on a number of factors, including the size and scope of the agency, its clientele, its location, and its financial performance. As a result, digital marketing agency owners must carefully consider all of these day to day operations before arriving at a valuation for their business. One of the most important factors in digital marketing agency valuation is the size and scope of the agency. Generally speaking, larger agencies will command higher valuations than smaller ones. This is because larger agencies tend to have more clients, more resources, and more name recognition than their smaller counterparts. Additionally, larger agencies are often able to command higher prices for their services due to their economies of scale. As a result, size is often one of the most important determinants of digital marketing agency worth. Another important factor in digital marketing agency valuation is the agency's clientele. Digital agency owners should carefully consider the types of clients they serve before arrives at a valuation for their business. Generally speaking, agencies that serve large, well-known brands will command higher valuations than those that serve smaller or less well-known brands. This is because large brands are often willing to pay premium prices for high-quality digital marketing services. Additionally, serving large brands can help an agency to generate positive word-of-mouth and build a reputation as a top-tier digital marketing provider. As a result, the quality of an agency's clientele is another important determinant of its value. Finally, digital marketing agency valuation also depends on the financial performance of the agency. Agency owners should carefully consider their long term revenue growth and profitability when arrived at a valuation for their business. Generally speaking, companies with strong revenue stream more growth and profitability will command higher valuations than those with weaker financial performance. This is because investors tend to be attracted to companies that are growing rapidly and generating healthy net profit margin. Additionally, companies with strong financial performance are often seen as being less risky investments than those with weaker financials. As a result, financial performance is another key factor in digital marketing agency valuation. Standard service business valuations apply to most marketing companies, including digital agencies servicing content marketing, SEO, link building, website design and PPC management team. In such cases valuations can range from 3x to 5x of EBITDA (earnings before interest taxes, depreciation & amortization) or SDE (seller's discretionary earnings). That's a big range. Most businesses are going to fall on the 3x side of that range for several reasons:

Investment Risk

Significant buyer investment risk exists for investors looking to acquire digital agencies. While good buyers have the vision to see opportunities, they also will have a keen and often overcompensating view of the risks associated with making an acquisition. These risks discount the value of any investment in a private business. Here are just a few. First, market risk can and will impact the value of a business. The recent pandemic is the perfect example of how outside forces can greatly and immediately have a negative impact on the value of your agency. This is often called systematic risk.

Second, small or smaller private companies always include a discount to value because they do not hold the same liquidity preference premium held by public companies. Public companies often hold more sustainable and scalable income, but more importantly, they are liquid. Liquidity means shares can be more easily bought and sold in an active market between two willing buyers and sellers. Third, internal business decisions risk. There is inherent business risk within the operations and individual market of a given company. This is often referred to as idiosyncratic risk. Liquidity risk, systematic and idiosyncratic risks will all serve to haircut your company's value, especially when compared to the next best long term investment opportunity.

Cost of Capital

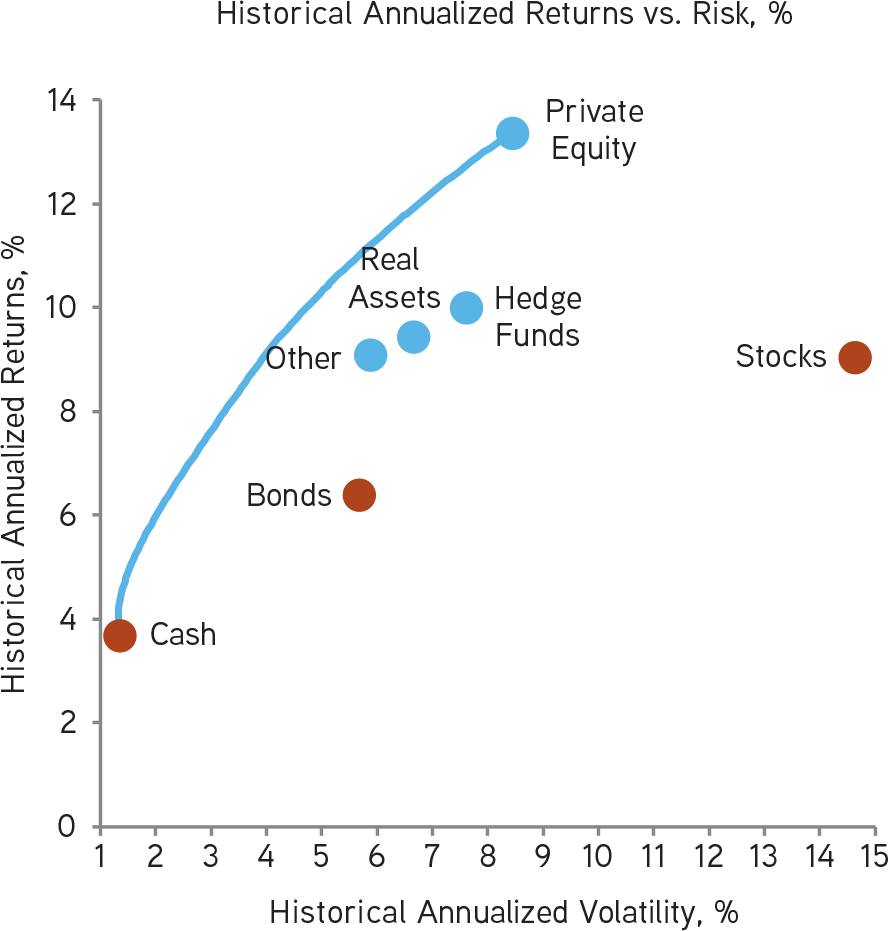

The cost of capital in digital agency mergers and acquisitions is more than just the interest rate of the debt used to acquire the business, which can range from 5% to 20%+, depending on the source and type of capital used (mezz financing can be double the cost of senior debt). When buyers assess the cost of capital, they also typically take into account comparable "next best investments. If I'm doing a comparison as a buyer, I might look at it like this. I have $1M to invest in something. In this case, I would compare it against three separate options:

- Buy public stocks or bonds.

- Buy real estate with rental income potential.

- Acquire a digital agency.

While these are not apples-to-apples comparisons in their risk profile and liquidity, performing this exercise is helpful in determining whether buying a particular business or business asset will be a good investment. The following chart provided by KKR do a great job comparing the risk/return profile among various asset classes.

In our case, we might ask:

If I were to invest my $1M in a digital agency valuation vs. public stocks or real estates, would my increased return on investment greatly overcompensate me for the increase in comparable risk.

Acquiring a digital agency has significantly more concentrated (non-diversified) risk than simply buying a mutual fund or buying rental properties. As such, the return on investment should greatly overcompensate for the comparable risk. Most sellers don't consider this in their own value calculations when it comes to selling their businesses. Let's use an example to compare. Let's say your digital agency is producing $1M a year in EBITDA. The seller wants $5M for the business. You might say,

Well, that's a great investment! I'm getting 20% return year-over-year on my money! That'll beat my current stock portfolio.

However, the risk profile and capital cost is significantly higher in this private illiquid investment than in public stocks or even private real estate, especially if the acquisition is financed with debt (which is very often the case). In addition to the opportunity cost, the cost of capital itself (e.g. APR of acquirer senior and subordinated debt) will also play a role in how to determine the value and willingness to pay in an acquisition. We'll get to that a bit more in-depth shortly. A seller might say,

But, my business has so much potential! If you do X, Y or Z, it will double. I know it! When it does the buyer will be the recipient of all those gains!

Buyers rarely pay a seller for such potential unless you're selling a product business ( not a service) business to Facebook. And, that's not going to happen here. If you consider the long standing risk profile, cost of the capital itself and the opportunity cost of the next best investment, higher valuations rarely compute for a savvy buyer.

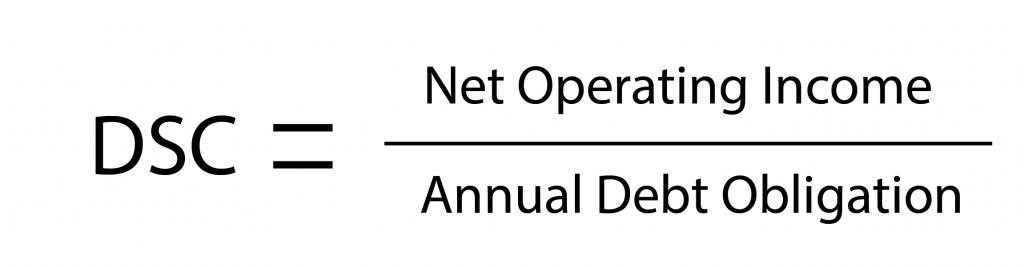

Debt Service Coverage Ratio

Let's continue with our previous example of a $1M EBITDA company looking to sell for $5M. I like to compare such instances using the SBA 7(a) loan program to see if the deal is even fundable. In SBA 7(a) financing, debt service coverage (DSC) is the way SBA loans are stress-tested based on historical income. Debt service coverage is computed as follows:

The SBA requires a minimum debt service coverage (DSC) ratio of 1.5x on a monthly basis. They prefer 2x debt service coverage. While today's interest rates make the cost of capital in the numerator above less than historical averages, most assumed valuation process do not meet the 1.5x threshold. The best rates on smaller M&A transactions today are what buyers can get from the SBA. In that case, we're talking about somewhere in the 7% APR range. At a $5M, 6% annual interest (which is very low) and a 10 year AM schedule (typical for SBA), the monthly principal and interest is roughly $55K. If we throw that into our annual DSC calculation, we're looking at DSC=$1,000,000/($55,000x12)=1.51 In other words, we can barely even finance the deal at a $5M valuation, assuming historical income and the fluctuating interest rate will continue forward at their current levels.

How to Bolster the Value of Your Digital Marketing Agency Worth

In order to boost the value of your digital agency, you'll need to make it both scalable and sustainable. Scalability and sustainability require one or more of the following:

- Consistency of Revenue. How consistent will the revenue be into the future potential? Historical revenues are typically used as a barometer for future performance, but what do those prospects look like? How will the agency continue to achieve similar (or better) historical sales revenues with new owners in place? How are you preparing for that reality?

- Recurring Income. Consistent, recurring income--particularly those under contractual obligation to pay a given amount--is what high-value digital marketing agencies are made of. It's one of the reasons we moved to managed SEO services.

- Growth of Revenue. You can't just say your business will continue to revenue increase. It has to be a foregone conclusion. What avenues are currently being utilized for new client acquisition? Is that growing? If not, what

- Diversity of Revenue. How diverse is your customer base? How many of your top clients make up more than 10% of gross revenues? What can you do to further diversify your satisfied customers base? Can you diversify by adding on ancillary, but complimentary services like we did with our blog writing service? (which also bolstered recurring revenue)

- Integrity of Process. Are your revenues sustainable? Are you adhering to industry-standard guidelines or is your business built on flash-in-the-pan tactics to make a quick buck? Sustainable revenue means integrity of process.

- Systems, Processes and Standard Operating Procedures. Sell-able businesses include teams of people who can operate the business regardless of who is at the helm.

In other words, you'll be aiming toward creating a real business, not a one-man shop. Real businesses include quality team members and systems and different processes that create reliability of services and outcomes for lifetime client. The implementation of such standard operating procedures ensures the business itself will exist long after any single owner has had his/her hands on it. Because we have worked as both buyers and sellers of businesses and because we provide a white label SEO service to other SEO company entities, we know a thing or two about what it takes to build, run, buy and sell a digital agency. We would love to connect with you and your leadership team regarding your next transaction and how we can help with our SEO service. Get in touch!